Find out the webinar replay of the “Market review of environmental impact claims of retail investment funds in Europe” presentation by Nicola Koch, Head of Retail Investing, and David Cooke, Law and Policy Lead at 2DII, available here.

We have gathered sufficient evidence to show that there is a high unsatisfied demand from European retail investors to have a real-world impact with their investments (varying between 35-65%[3]), while most impact-oriented investors are likely willing to sacrifice returns to achieve this objective.[4] At the same time, studies showed that most retail investors expect real world impact from finance products which are labelled as “green” or “sustainable”, however, the majority of them cannot detect impact-washing without external support.[5] Although the ESAs echoed our assumption that the European Unfair Commercial Practice Directive (UCPD) might be applied to environmental impact claims of financial products, we still expect that the current regulatory framework is not fit for purpose to effectively address misleading environmental impact claims in the financial sector.[6] Without legal enforcement and regulatory changes, financial institutions have a strong incentive to exploit the demand for financial impact products by selling low-impact products with misleading impact marketing claims. This implies a high risk of misallocation of capital flows towards financial products with low potential to contribute to the European climate goals, reputational damages, and legal penalties as well as increasing investor mistrust.

In fact, after we documented the misuse of environmental impact claims in 2020 and 2021[7], this market review confirms the persisting use of misleading environmental impact claims, also after the implementation of SFDR. Our research objective was to assess current environmental marketing claims as found in marketing materials related to retail funds across Europe based on the updated UCPD guidelines. We filtered the Lipper fund database for the 454 largest environmentally focussed Art 8 and Art 9 funds (in terms of AUM) for which marketing documentations were readable in either English or French. Our headline results are as follows:

- 27% of all in scope funds were associated with environmental impact claims. No fund with an environmental impact claim could sufficiently substantiate its claim according to the updated UCPD Guidance indicating a substantial potential legal risk.

- Over 2/3 of funds with environmental impact claims were classified as Art 9 financial products according to SFDR.

- Of the environmental impact claims deemed to be false or generic, there were 3x more appearing in Art 9 fund marketing materials compared to Art 8 fund marketing materials.

- Most environmental impact claims deemed false equated “company impact” with “investor impact”, most environmental impact claims deemed unclear were not substantiated by sufficient information and most environmental impact claims deemed generic were fund names including the term “impact” with insufficient additional information.

- Our findings reveal a high number of misleading environmental impact claims in legal documents (including SFDR disclosures) and commercial marketing materials.

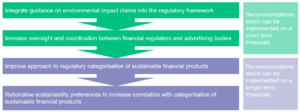

We propose a menu of short-term and longer-term recommendations to address systematic impact-washing risks:

About our funders: About our funder and the project: This project is funded by the LIFE Programme and it’s NGOs on the European Green Deal (NGO4GD) funding program under Grant Agreement No LIFE20 NGO4GD/FR/000026.

![]()

The paper is part of the Retail Investing Research Program at 2DII which is one of the largest publicly funded research projects about the supply, demand, distribution and policy side of the retail investment market in Europe.

[1] See e.g. 2DII (2017); 2DII (2019); 2DII (2020a); 2DII (2020b); 2DII (2021); 2DII (2022a)

[2] See EBA (2023), EIOPA (2023); ESMA (2023)

[3] See 2DII (2022b); 2DII (2023)

[5] See 2DII (2020a)

[6] See 2DII (2022a)

[7] See 2DII (2020b); 2DII (2021);